Table of Contents

Background Context

Low-income families with income less than $2,500 a month may face a significant challenge in budgeting, especially in 2025 when inflation and the standard of living will be high. Unfortunately, recent statistics show that an average single adult in America spends about $1000 to $1500 a month on basic needs- house, food, transportation, among others, and sometimes more in costly cities. Every dollar is consequential to families whose monthly incomes are less than $2,500.

Many families are forced to juggle rent ranging between $750 and $1,200 per month, depending on the place of residence, food costs in the range of $300 to $400 per month, and other bills, which amount to approximately $400, and all that requires narrow planning and limiting expenses. The following are five viable, realistic ways to make even that tight budget work, start saving, and alleviate financial stress using both commonly available practical tools and techniques.

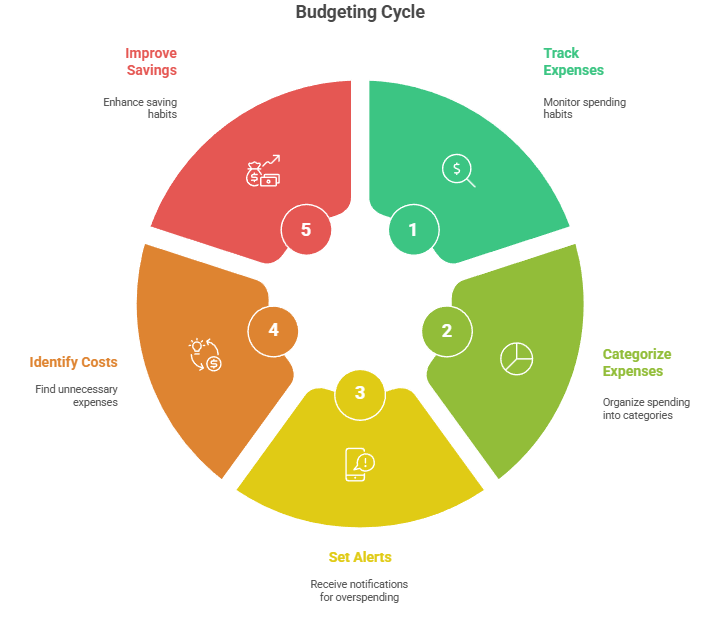

1. Track Every Dollar Using Free Budgeting Apps

A very effective and easy way of avoiding excessive spending is to strictly trace the whereabouts of every single dollar. Popular Free Budgeting apps like Mint, EveryDollar, and Goodbudget are programs that allow you to add income and expenses with a few clicks. As an illustration, when rent is $900 per month, groceries $350, utilities $150, and transportation $200, the applications will show a graphical view of the remaining $900, which can be used on other activities.

The expenditure tracking will show patterns and waste better than recollection itself, and will warn you if you give yourself a limit in any category. Costly habits, including common restaurants, can be recognized and experienced so that low-income families can redistribute the funds to essentials or savings goals as a result of these applications.

2. Optimize Grocery Shopping with Smart Planning

Food expenses, also kept at about $300-$400 a month on average by the low-income families, may easily get out of control without being planned out. Savings: Meal planning, shopping list compilation, and discounts/coupon usage can result in significant savings. An example of this is that by substituting name-brand products with your own store brand, you can save 15 to 25 percent on a typical grocery bill.

Buying in fishy stores like Aldi or Walmart would save a lot of money. Purchasing in large quantities lowers the cost per meal of such staples as rice, beans, and frozen vegetables. Using digital tools like Ibotta, you will also be able to earn cash back or other discounts on groceries.

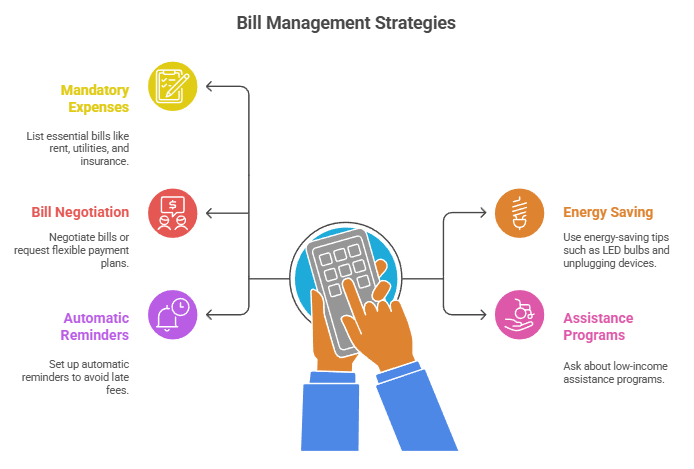

3. Prioritize Essential Bills and Negotiate Where Possible

The $2,500 income is taken by housing, utilities, and insurance, which take a large chunk. No priority should be given to late rent or mortgage payments, which are usually about $700 to $1200, the main reason why a person can avoid late charges and eviction. Utilities can be as high as an average of one hundred and fifty dollars per month; basic energy-saving steps, like installing LEDs, disconnection of devices when not in use, and minimizing the use of HVAC systems, can be used to reduce the costs.

Do not be afraid to call service providers, such as internet, cable, and utilities, to enquire about payment owing plans, or low-income programs. Most utilities assist in terms of discounts or longer duration of paying bills to eligible families, hence reducing monthly cash flow.

4. Build an Emergency Fund Gradually

It might seem small to save at least $10 a month, but it builds up over time and helps in providing a financial buffer against any unexpected incidents, such as the need to repair a car or meet the costs of a medical visit. Making this an automated process with the help of banking apps or similar round-up savings apps like Acorns (which round transactions to the nearest dollar and provide protection to the remainder) simplifies the work.

E.g., by saving $10 a month, one will save $120 a year, thus reducing reliance on a payday loan or credit card. This is necessary to be financially stable, not only because the average price to have a car mended is between $400 and $600, but also because medical copayments may also worsen the situation in a short period of time.

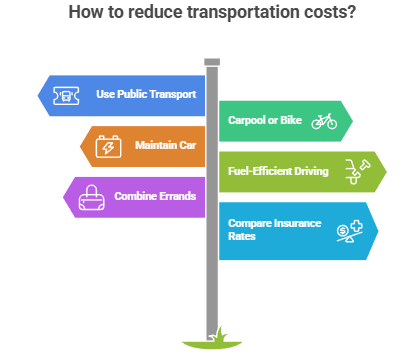

5. Reduce Transportation Costs with Smart Choices

Depending on the type of transportation used, transportation expenses are estimated at approximately $200 a month for a low-income family, which includes fuel, transit, and insurance. The use of public transport can save money by 40 to 60 percent of that spent on cars, where possible. When commuting is not viable, car-sharing or bicycling will reduce gas and fuel, and maintenance costs.

Regular maintenance of the vehicles also helps avoid expensive repairs. Enabling the scheduling of errands efficiently, such as making multiple trips and avoiding rush hours, can save many gallons of gas per month. In addition, shopping for cheap insurance plans also helps more in cost reduction; the premiums go as low as $600 to $1,200 per year.

3 thoughts on “5 Budgeting Hacks for Families Earning Under $2,500”

Comments are closed.