Table of Contents

Background Context

To achieve financial stability that can last a lifetime, personal budgeting is the key to achieving the financial stability of American families whose income ranges between $4000 and $7000 every month. By 2025, middle-income households will be faced with the constant rise in the cost of living, insurance premiums, and changing lifestyle conditions. Based on the current household budgetary aspects in the United States, families in this income bracket use an average of $1,500-2,300 on housing, $600-$800 on groceries, and $800-$1000 on transportation and utilities on a monthly basis. It is necessary to set up useful and strict budgetary regulations to achieve a balanced relationship between current demands, non-essential desires, and savings in the long term. Based on best practices in the industry and current standards of expenditure, the following ten rules can assist middle-income families in monitoring their spending, maximizing their spending, and improving their financial well-being.

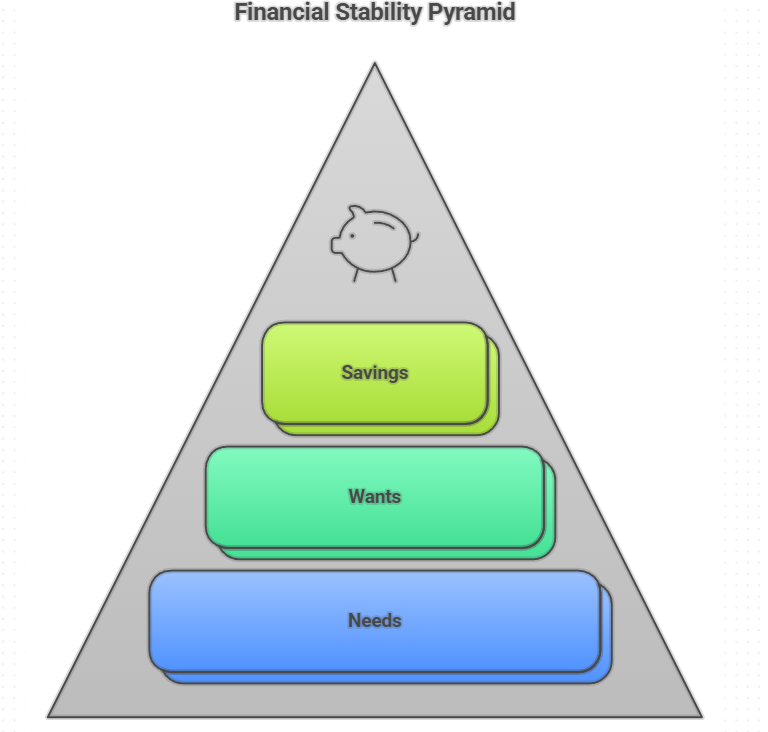

1. Use the 50/30/20 Rule as Your Baseline

Divide your monthly after-tax income (est. $6,000) into 3 broad categories: 50% ($3,000) needed, 30% ($1,800) wants, and 20% ($1,200) savings and debt repayments. This strategy keeps the family finances on a level, ensures the needed spending, and encourages the constant increase in wealth.

2. Track Spending with Digital Tools

Keep a close account of all the dollars with the help of applications like Mint or YNAB (You Need a Budget), or Personal Capital. Set hard monthly budgets, e.g., grocery budget of $700, eating out of budget of $300, and utilities budget of $400. Monitoring through data will show the behavior of spending and thereby avoid excesses, which is crucial in families dealing with mortgages, insurance, and childcare, among other recurrent expenditures.

3. Set Automated Savings to Build Wealth

Automatically redirect up to 10 -20 per cent of income ($400 -$1400 annual) to high-yield savings, a 401(k), or other investments. With a fluctuating monthly cash flow, regular contributions should then take priority, and then one can commence spending discretionally.

4. Cap Housing at 30–35% of Income

Cap rent or mortgage payments recommended at 35 per cent of take-home pay, including taxes and insurance. At a monthly income of $5,000, this limit translates to a housing cost of $1,750 or even less. In case strategic downsizing or refinancing will decrease this amount, direct the amount to savings or enrichment activity designed to benefit the family.

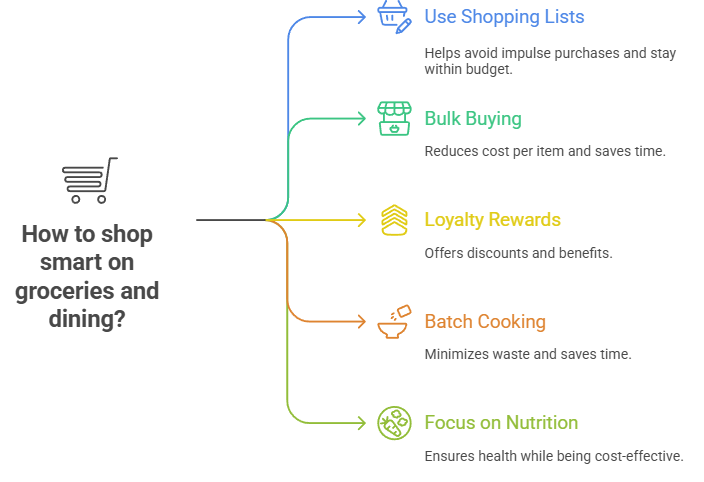

5. Shop Smart on Groceries and Dining

Limit groceries to less than $800, and limit restaurants to less than $250-$350 a month. Use shopping lists, bulk buys, and reward cards to save money on food. Freezer meals help to extend the life of a purchase, and through batch cooking, waste is minimized.

6. Prioritize Health and Insurance

Spend no less than 10% of monthly earnings (400-700) on health insurance, out-of-pocket care, and preventive drugs. Annual comparison of plans, use of health savings account (HSA), and keeping policies active without expiration.

7. Manage Transportation Efficiently

Limit car monthly payments, car insurance, car fuel, and maintenance to less than $900. Use the bus or ride share where possible, and get your vehicle serviced regularly to prevent unnecessary expenses of fixing your car.

8. Limit Recurring Subscriptions and Impulse Spending

Perform audit and cancellation of unused streaming services, memberships, and subscriptions. Place a limit on entertainment and shopping spending at night: limit adults to spending $ 150 a month on fun money. Take credit cards that have a cashback or rewards program, and pay balances once every month in order to save on interest.

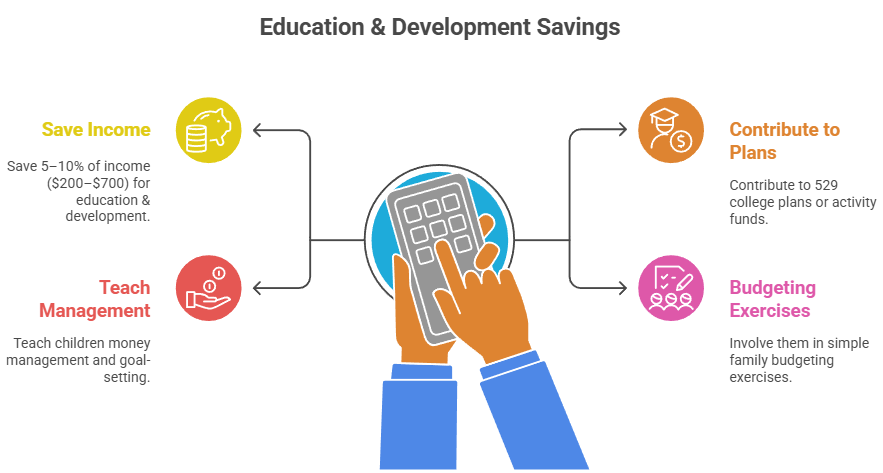

9. Prepare for Kids’ Education and Growth

Allocate 5 -10 per cent of monthly earnings ($200-$700) towards education accounts like the 529 college savings or after-school programs. Integrate children in saving goals, therefore instilling proper money habits in them at an early age.

10. Build Robust Emergency and Sinking Funds

Plan a store contingency fund at least 36 months’ worth of expenses, that is, about $15,000 to $30,000 to save against the unexpected. Break up the savings objective into small monthly savings installments with the help of auto-deposits and hardworking money-market or savings deposits.

3 thoughts on “10 Dynamic Middle-Class Budget Rules for $4,000-$7,000/Month”

Comments are closed.