Table of Contents

Background Context

Couples with earnings that are 7500 dollars and above, paying a dual income per month in 2025, have a unique financial strain and opportunities. Latest figures prove that these households normally spend at the figures of $2,200 to $2,800 per month on residence, $800 to $1,000 per month on food, and transportation and utility at $900 to $1,200. An effective budget will help these couples to balance necessary living costs, desires in life, investments, and long-term financial security, and minimize stress. Customized budget plans enable a couple to optimize revenue, have a long-range program, and observe sound fiscal discipline.

1. Establish Clear Communication and Joint Financial Goals

Being open and truthful when it comes to earnings, debts, expenses, and priorities is a prerequisite. The goals can be joint in nature: one might want to save $12,000 in the twelve months and then use this sum to put a 20 percent down payment on a $144 thousand home, or contributions to the retirement, or the school fees. The same financial vision encourages accountability and togetherness. However, monthly financial meetings should also be scheduled to ensure clear and solid conversations.

2. Use a Modified 50/30/20 Budget Rule

As an example, a joint net income of $9,000 can be divided into the following amounts: needs, including housing, food, insurance, utilities; wants, including dining out and entertainment; savings and debt repayment with 50%, 30% and 20% respectively. This moderation strategy would see necessary needs met, but spending and future wealth accumulation will be a priority.

3. Automate Savings and Investment Contributions

Automation of savings of not less than 20% every month facilitates financial success. The use of the surplus funds should be mainly focused on maximizing the deposit in 401 (k) (up to $23500 each person in 2025), into Health Savings Accounts (family limit before that is $8550), and into regular taxable investment accounts. Automation has the effect of reducing decision fatigue and promoting steady wealth building, irrespective of variations in monthly income.

4. Track and Categorize Spending Monthly

With the assistance of applications like Mint, Personal Capital, or Tiller, it is possible to track the spending patterns precisely. Classifying the expenses will assist in realizing overspending, where most of these are subscription creep or a huge amount in dining out that is beyond the limit of $600 per month. Rerouting of such funds towards decrement settlement or investments enhances greater financial health on a long-term basis.

5. Allocate Separate and Joint Accounts

The dual-income couples have the advantage of having a joint account, which they use in meeting their fixed costs; mortgage, about $2,500, utilities, about $350, groceries, about $900, etc, but keeping a personal discretionary account. The process is an act that has a balanced share of responsibility among individuals and financial independence, as well as helps to decrease conflicts and promote disciplined budgeting.

6. Limit Housing Costs to 30% of Take-Home Pay

In case of mixed net incomes, which are greater than $7,500, housing costs must not be more than 30 percent (around $2,250 a month). It will be possible with refinancing, with moving, or negotiating a rental agreement. Housing rent savings can be diverted to an investment account or family recreational activities, thus increasing the quality of life without jeopardizing the financial well-being.

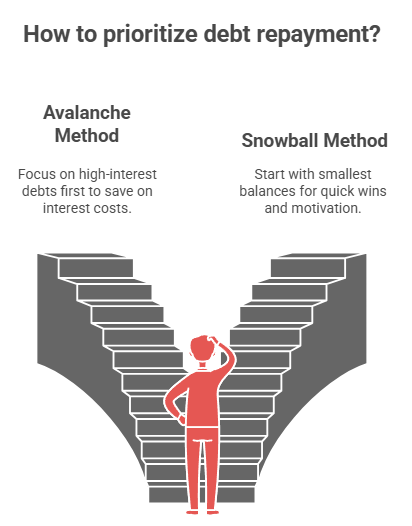

7. Prioritize Debt Repayment Strategically

Devote at least 10% of income ($750+) to clearing high-interest debts, e.g., credit card, student loans, or auto loans. Make use of debt-reduction programs like the snowball technique (paying off the smallest debt first) or the avalanche method (paying off the largest debt first) to make the debt repayment process quicker and decrease financial liabilities.

8. Plan for Emergency and Large Annual Expenses

Establish an emergency fund consisting of 6 months of living expenses, which is generally approximately, six months of living expenses, which are around $30,000-$7500 income households in the category of $7,500 and above earn, amounting to a $30,000 30,000-emergency fund. Set up sinking funds to offset annual lump-sum costs such as insurance payments, property taxes, or vacations by saving out $300-$500 a month in special accounts. This saving will cushion financial shocks and ensure that they have peace of mind.

Additional Tips and Resources

- Utilize domestic budget models. Expense categorization and visualization can be simplified with the help of such tools as an Excel-based or Google Sheets budget tracker (sample templates could be found online).

- Review budgets quarterly. Reflect lifestyle changes, changing incomes, as well as financial objectives.

- Leverage tax advantages. Minimize the liability by the maximum possible amounts of deductions and credits; refer to a financial advisor or tax software.

- Involve the whole family. Financial literacy can be taught in the long term by teaching healthy money habits and involving dependents in family finances.

2 thoughts on “8 Smart Budget Plans for Dual-Income Couples Earning $7,500+”

Comments are closed.