Background of Thematic ETFs in the U.S.

Thematic and alternative ETFs – all these AI and clean energy subjects, crypto and options exposures and strategy/ alternative exposures are now core positions within a portfolio.

Burnishing product devising, high investor bi-polarity finding of concentrated exposure and futuristic exposure, lately altered regulatory/structural reforms are transforming the ETF investing industry. Expenditures are in the many trillions. In American asset management, liquidity of assets depends on shelf counts, proliferation and high flows of products.

Thematically/alternative trading ETF segments have encouraged the growth in the relatively new industry, reports that have reported that the set up of the new products/ETF AUM and the swift rates of product/ETF development are set to cause an expansion in thematic/alternative ETF products/markets.

Snapshot — size, scale and definitions of Thematic ETFs in the U.S.

- ETF industry assets (2025 context): U.S ETF industry assets are at a record high (translation: shows U.S. ETF industry assets are in the multiple trillions). Based on the definition cut, the 20242025 head line industry AUMs will be between +13 and $10. The grandest forecast of influencers’ headline approaching new outlets, it is stated, is cast not only by the largest trackers and consultancies, but comprehensively fulfilled by the middle of the year 2025.

- Thematic & alternative subset: A thematic choice, an alternative is an exceptionally new sub-universe. Per recommendations, the U.S themed ETF has hundreds of billions of assets, and the U.S themed share going around the world has hundreds of billions of assets, and gets listed on the thematic because the ETF raises the crypto spot ETF, it would be thematic in the stratosphere once more.

- Fund counts: Its U.S. listed ETF product eventualities are a thousand, outside of the U.S. thematic / alternative category eventualities are one thousand, and products eventualities are 4000 and 8000 respectively.

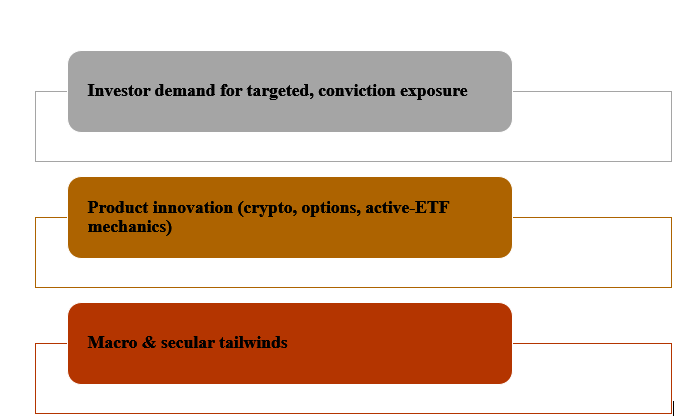

Key drivers behind the growth of thematic & alternative ETFs

- Investor demand for targeted, conviction exposure: Retail and advisor channel funds are becoming anxious about using ETFs to articulate single-conviction, no-one-stock risk. Thematic wrappers are easy to access and trade.

- Product innovation (crypto, options, active-ETF mechanics): The addressable market for spot crypto ETFs, options-based yield products and active ETF wrappers would grow in 2024-2025, introducing new flows and redefining thematic to many investors. Launches and inflows were triggered by the shifting way the SEC was treating commodity ETFs and the grouping of fresh product launches.

- Macro & secular tailwinds: Structural shifts, AI deployment, energy transition, demographic change create investable universes with long horizons, helping thematic stories survive short-term performance variance.

Risks, frictions and structural concerns

Labelling, overlap and “story risk”: Thematic ETFs can have considerable overlap with sector and factor bets; some are actually just a sector camouflage of a sector investment. The width of the investable universe and the overlap may not suit the investor adequately. According to Morningstar and others, most thematic funds should be seen more as story than a long-term approach.

Concentration & liquidity risk: Huge names can have the popular baskets under their wings. One of the likely results of strained markets is that liquidity that could lie on the theme mid/small cap stock constituents background could be suctioned out that will create a tracking and redemption flows. Systemic fears are compounded each time flows of assets within a theme reversed.

Performance dispersion and timing risk: Authorship performance is path-dependent-a themed-based path-dependent immobilization or lasting victor might operate considerably greater performance, yet for each theme-based investment activity that runs, an average buying underperforms or randomly experiences worse results through standard indexes. A majority of investors who follow recent winners record dismal dollar-weighted returns.

Regulatory and operational evolution: The new SEC product listing standards (e.g. commodity/ crypto ETPs) save time-to-market, but create a challenge of disclosure, custody, and investor protection. The rate of product approvals enhances innovation at the expense of unreliable tests on the product designs.

Implications for the alternative ETFs market and the wider U.S. asset management industry

Reallocation of distribution economics: ETFs, especially thematic and alternative ETFs and other ETFs, start displacing mutual fund assets; there is a danger that mutual funds will either have to launch new ETF share classes or change policies related to distribution to influence sales. The transformation alters revenue sources and shifts the focus of asset managers towards size and product-market fit.

New revenue models: Firms are monetising with similar products and are experimenting with complementary products- active ETFs, multi-asset wrappers, and thematic suites. Honesty can help the fee-strained managers merge business productiveness with product innovation.

Market structure effects: With a scale-linked price direction, the liquidity of underlying securities can be acquired by a thematic product of large scale. As the assets of certain thematic ETFs grow, market impact in portfolio formation and risk cancellation arises as a concern to the market makers and issues for Curated ETF issuers.

How investors should treat thematic and alternative ETFs

Use them as satellite exposures, not as core holdings: Thematic ETFs perk up the faith, but they ought to be applied on the grouping of core ETF investments.

Check index methodology and holdings overlap: Modify the prospectus and index construction policies- understand the concentration, rebalancing, and necessity of inclusion.

Be mindful of fees and liquidity: Very low expense rates are important, weighted by the expense, as the asset under management of the funds and the significance of the bid-ask and the volume per day, concerning cost and tracking of the execution are of paramount importance.

Avoid “story chasing: Compute the theme, the competitive environment, long-term feasibility, lots of fads not much welcome and seasonal.

Strategic moves for asset managers in the thematic & alternative space

Focus on governance and transparent indexing: Transparent methodology and licensure by third parties diminishes reputational risk and aids its uptake by institutional allocators.

Scale/distribution partnership: These clients can be reached by advisory platform and retail broker form companies at faster rates, AUM accumulation; asset managers need to sell a differentiated product together with a high-rate distribution.

Product stickiness through education: Considering the narrative risk, the effective sponsors allocate money to client education and message-oriented at the outcomes.

Forecast & outlook (next 3–5 years)

Continued growth but with consolidation and segmentation: Long term ETFs in general will only continue to rise; thematic and other alternative will grow but only those that will be successful are the assets that have an effective index system, carrying scale of implementation and distribution. In any event, this will increase through substantive proportional percentages in 2020s as projected by industry, though, geographically.

Active, crypto, and options-driven ETFs will be a material share of new launches: ETFs will form a high percentage of new launches. These divisions make up a prevailing percentage of product innovation due to regulatory clarity (specifically, commodity/cryptocurrency ETFs) and client enthusiasm.

Investor sophistication will rise: The quality of thematic product may also become unfavourable as low-quality thematic product may be funneled out by a superior quality offering building a solid base of capital.

Final verdict of Thematic ETFs in the U.S.

In the U.S., thematic and alternative ETF universe has developed out of experimentation of the boutique approach to establish appropriate pillar of the modern portfolio development. Supported by billions of ETF industry assets and thousands of listed securities, the sector growth is structurally anchored by investor demand, product creation and distribution transformation. With that said, thematic and alternative ETF investors should face one label risk, one concentration risk, and one execution risk, but these risks are further exacerbated when traffic moves rapidly into or out of concentrated baskets.

In the eyes of asset managers, confidence will go to those who integrate transparency in their index design, scale of operations, disciplined and measured distribution and investor education. Stated simply: thematic ETFs are not a trend; they are here to stay. However, they cannot substitute diversified core holdings. Instead, manage them like the tools of conviction they are, helpful, mighty, and capable of scaling to a larger extent so far as the investors and managers can handle their limits and come up with trade-offs.