5 Ways 2026 Tax Brackets Will Hit the Middle Class

Important Adjustments and Features

1. Bracket Inflation Adjustments

The Internal Revenue Service has increased all the tax bracket income thresholds to counter inflation, as well as to reduce bracket creep.

As an illustration, the 12 % bracket of single filers is now imposed on incomes between $12,401 $50,400, and the 22 % bracket is imposed on incomes between $50 401 $105,700.

2. Standard Deduction Increases

It will raise the standard deduction to $16100 as a single filer and to $32200 in the case of jointly filing married couples in 2026.

Heads of household have a right of $24,150.

Further, an increased deduction is given to taxpayers 65 years and older, which is an addition of an extra six thousand dollars in some situations, and which has phase-outs under the Omnibus Budget Law through the Balance Adjustment (OBBMA).

3. Top Rate & Bracket Thresholds

The maximum marginal rate of 37 % still stands, but now has a beginning point of $640,600 when a person is single and $768,700 when it is married. Other brackets like 35%, 32%, 24% etc. have been indexed slightly upwards according to inflation.

4. Permanent Extensions & New Provisions under OBBBA

OBBBA also contains many tax cuts that were passed first in the 2017 Tax Cuts and Jobs Act (TCJA), and the original expiration dates of which were 2025. It also brings in new deductions, including deductions on tips and overtime, increases the maximum tax credit on salary (SALT) deduction to $40,000 (phased out), and increases existing tax credits.

What “Middle Class” Means in 2026 & Who Is Affected

The term middle class is not strictly defined, but in computing the effects of taxes, the term usually covers incomes of households having incomes that will be taxed between, say $40,000 and $250,000, depending on the place of residence, family size, and the amount that is deductible. These families generally fall within the 12%, 22%, 22% or % 24% bracket and sometimes even go close to the 32%. Since 2026, bracket conditions and deductions have been changing up and down, and since many people in the income bracket will be affected, whether positively or negatively, their marginal and effective tax rates will change.

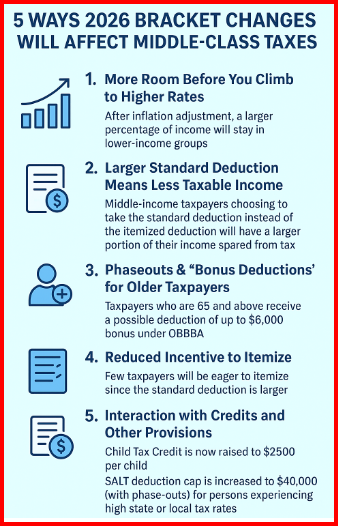

5 Ways 2026 Bracket Changes Will Affect Middle-Class Taxes

Through the following, the middle-class Americans can be said to be affected by these changes:

1. More Room Before You Climb to Higher Rates

After inflation adjustment, a larger percentage of income will stay in lower-income groups. Middle-income earners will have much more income to go to until the 22% or 24% bracket, and thus the effects of inflation will be cushioned.

An example of this would be a single filer making between $60,000 in 2026 will first pay 12 % on amounts less than $60,000, and then 22 % on the rest, but the eligibility to cross over to 22 % is stiffer as compared to the old years, and this will decrease bracket creep.

2. Larger Standard Deduction Means Less Taxable Income

Under the improved standard deduction, middle-income taxpayers choosing to take the standard deduction instead of the itemized deduction will have a larger portion of their income spared from tax, thus leading to a reduction in effective taxes. The case in point is the example of a single filer whose gross income is $60,000 (which will decrease to $16,100 on gross revenue), and his income will be deducted more from his taxable income, which will save him or her taxes on a higher amount of money.

3. Phaseouts & “Bonus Deductions” for Older Taxpayers

Taxpayers who are 65 and above receive a possible deduction of up to $6,000 bonus under OBBBA, but it factors out as they earn more. This provision may be of benefit to middle-income seniors, especially.

However, individuals who are close to income levels will lose their eligibility or face a lack of full phase-outs, which will cause sharp cuts in tax reliefs.

4. Reduced Incentive to Itemize

Few taxpayers will be eager to itemize since the standard deduction is larger. Such a change can have an impact on the worth of the deductions, including the mortgage interest and state taxes, as well as the amount of the charitable contributions, which could reduce the value that used to be obtained by some middle-income homeowners.

5. Interaction with Credits and Other Provisions

OBBBA increases or does not increase various tax credits that apply to families with middle incomes:

- Child Tax Credit is now raised to $2500 per child.

- SALT deduction cap is increased to $40,000 (with phase-outs) for persons experiencing high state or local tax rates.

- There are new deductions created regarding tips and overtime compensation, to the benefit of the salaried workers whose payment is variable.

Taken together, changes can subsidize a portion of the tax bill, especially for those families that have children or families that pay large state/local taxes.

Risks & Possible Challenges

- Phaseout “Cliffs”: Persons with earnings above certain levels can find a rapid loss of benefits.

- State & Local Interplay: The states may not always keep up with these federal changes, and state taxes would be free to increase.

- Less Reward for Itemizers: Filers who can deduct a high deduction amount (homestead) might have less value in their itemized deductions.

- Inflation vs Wage Growth: An increase in wages may not entirely protect purchasing power if the growth fails to match the inflation.

- Future Changes or Repeals: Some of the provisions offered by the OBBBA, e.g., bonus deductions and extra credits, might be provisional or can be changed by legislation.

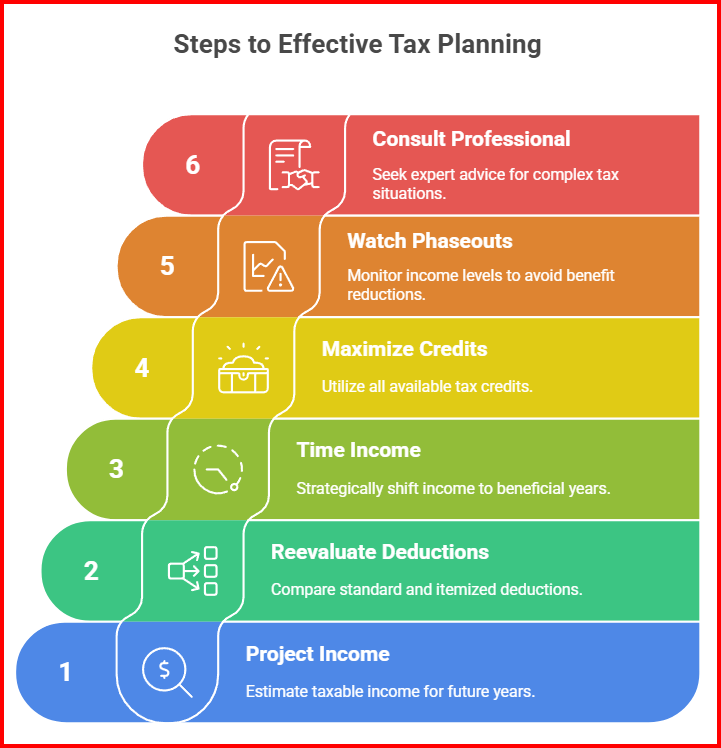

What Middle-Class Taxpayers Should Do Now

- Run a 2026 projection: Tables and deductions are updated, and taxable income is projected.

- Reevaluate itemizing: Check the standard deduction with those that are itemized in order to consider the most beneficial.

- Time income realization: Where possible, move the income of deductions to more advantageous years.

- Max out credits: Check all child tax credits, overtime, and tips deductions, and additional credits.

- Watch phaseouts: Be careful at the point of the income where the benefits can be reduced quickly.

- Tax planning with a professional: This is recommended, especially where there is a bracket cut-off or when the deduction structure is very complicated.

Final Thoughts

The proposed changes in the 2026 U.S. tax bracket- with inflation adjustments and OBBBA- are meant to ease the burden on people fighting the increasing cost. To most in the middle class, such changes provide breathing room: more income cushioned before being subjected to rising rates, an increased standard deduction, and increased credits.

The design is, however, delicate. There will be more beneficiaries of the tax system than other taxpayers, and those who are near the thresholds can have certain sudden changes. The medium taxation of the middle classes will become more of a balancing trade-off.

A careful consideration of tax planning and greater awareness will be mandatory in 2026. Look at the new IRS tax tables of 2026, compute personal changes, and make changes accordingly on financial decisions.