Table of Contents

1. The Fed’s Cautious Stance: What It Means

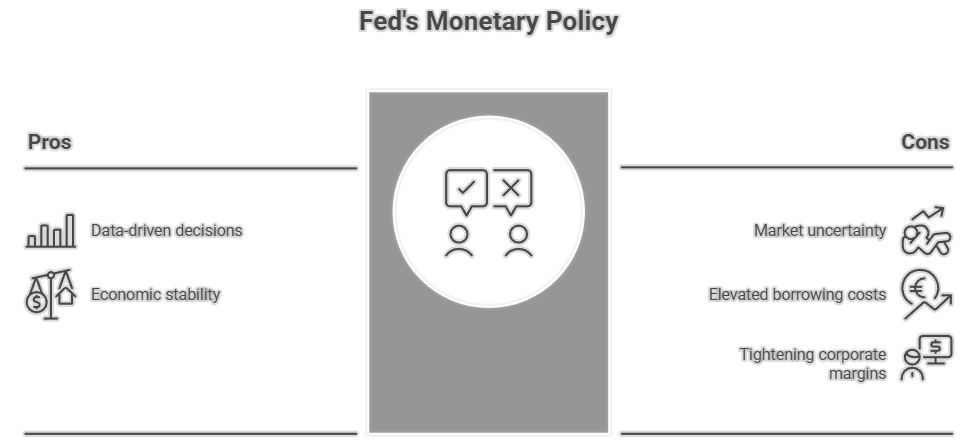

According to the minutes of the Federal Open Market Committee, almost all the respondents expect several reductions of the rate during the current calendar year, while keeping an eye on the employment rates, inflation rates, and the financial markets.

Although the markets are expecting accommodative policies, the Federal Reserve expressed an idea that they will not rush, and they will also be ready to revise the monetary policy in the future on the basis of information available.

To conclude, the Federal Reserve is not sending a message of a rapid reduction of the rate, but a conditional curve. This uncertainty creates market uncertainty; in the event of an underperformance in data, it may cause the reserve to delay taking any action, hence continuing on higher borrowing expenses than many may have predicted.

In the case of corporate parties, especially those that are highly leveraged or interest rate sensitive, e.g., growth-technology companies, this will equate to compression in margins and the reduction of the upside with financial engineering approaches.

2. Corporate Earnings: Good So Far, But Slowing

Although most of the corporations in the U.S are still recording higher than expected profits, the growth rate is slowing down. When considering the so-called Magnificent Seven technology names, the example of a slower growth rate beneath the wider range of the S&P 500 is obscured.

According to the quarterly report issued by Fidelity, the forward price-to-earnings ratios in the United States are still very high compared to their long-run average. This means that the markets are valued on high positive news and thus more susceptible to possible contradictions of the optimistic news.

The risks of pullbacks are increased when earnings underperform compared to high expectations and when the valuation levels are high. This is a relationship that contributes to the investor sentiment, as it shall be addressed below.

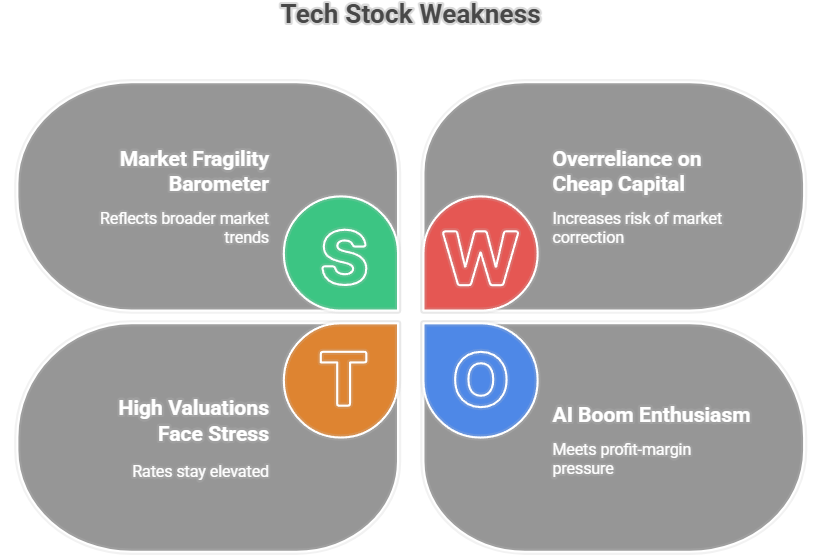

3. Tech Stock Weakness Comes Into Focus

Technology companies with high valuations have been doing well, but their margins are becoming smaller. Having higher valuations and increased interest in interest-rate changes and growth expectations, the technology industry becomes riskier with a reserved Federal Reserve market policy and with a slowing growth in the earnings climate.

Analysts have come to express concerns that the bubble talk is no longer a stretch by overvaluation; the narrative of the fear of missing out has become part of today’s talk.

Primarily, as the interest rates stay higher and earnings growth decelerates, technology stocks could be at the front of a subsequent correction as they are valued with further high growth and cheap financing.

4. Fed Policy Risk: A Hidden Pressure

We tend to describe the Fed policy as being hawkish or dovish, but the greatest risk is the uncertainty over policy direction. The very minute point to the increased risks of downside employment.

This makes it difficult to model for investors:

- Will the Fed reduce earlier or later?

- Will there be a re-acceleration of inflation?

- Will the labor market become weakened?

Such uncertainty increases premiums on risks and may narrow the valuations instead of widening them, particularly the businesses that need favorable monetary conditions (e.g., growth or technology companies).

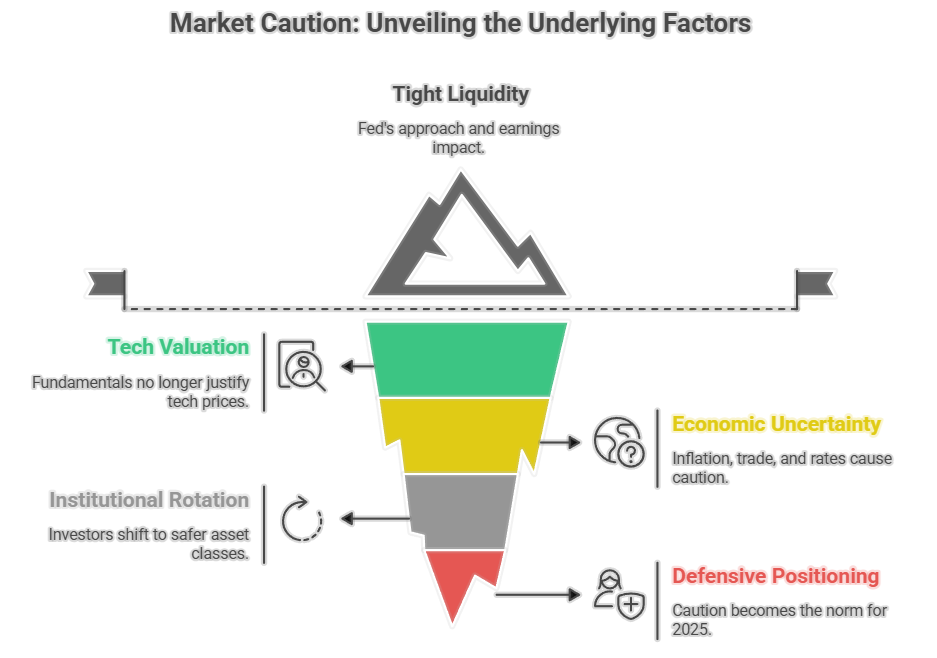

5. Investor Sentiment in the U.S.: Turning Defensive

The tone of the investor is changing to no longer be about growing anyhow, but rather which companies can endure stiffer conditions. U.S. Bank cited recent remarks as stating that, although equities recovered in 2025, investors are increasingly putting more emphasis on fundamentals than momentum because of tariff threats and increased volatility levels.

Sentiment is even more important when valuations are high, at which point Federal Reserve uncertainty and declining earnings would easily transition sentiment into risk-aversion.

6. Synthesis: Why Wall Street Is Turning Defensive

Putting all this together:

- The Federal Reserve has been hesitantly positioned, thus limiting growth-based companies by keeping their borrowing rates high.

- Growth in earnings is positive and slowing down, and therefore creates less surprise to expand another round of valuation growth.

- Technology valuations are too far-fetched and now vulnerable to more difficult macro conditions.

- Policy risk. Monetary policy risk is high, as is fiscal policy risk, which reduces the error margin.

- The sentiment is shifting towards becoming risk-aware rather than risk-on, and investors grow defensive.

Therefore, the war story of Wall Street is not a sensational one; it is a mindset that the market realized that all would not go up as high this time, rather what names would mature in more adverse situations.

7. What Should Investors Do?

The following are the practical lessons:

- Pay emphasis on quality: The companies that have high balance sheets and free cash flow regularly are expected to fare better within the environment of higher rates and slower growth.

- Question ratings: Forward price to earnings ratio is higher; this decreases the error level.

- Diversification in sector: In case technology is more visible, look at sectors that are less reliant on cheap money.

- Keep an eye on the communications of the Federal Reserve: Federal Reserve meetings in the coming few would determine interest-rate expectations and market positioning.

- Expect fluctuation: With a change in sentiment, even strong firms can fall into the deep due to opposite macro-economic shocks.