Table of Contents

Background Context

The ability to earn more than $10,000/month leaves a lot of wealth-building opportunities and also requires complex financial planning. In 2025, the high earners also face different sets of problems, which include coping with a complex tax bracket with federal marginal rates of between 32% and 37%, accessing equity compensation based on stock options or restricted stock units (RSUs), and deciding how to spend their money on discretionary luxury versus making wise investment decisions. Recent statistics show that the average expenditures incurred by this segment are about $3,000 to $4 500 per month in housing, $1,000 to $1,200 in groceries, and a huge surplus spending more than $2,000 a month. It requires sophisticated budgeting techniques to maximize savings, lower taxes, and build long-term sustainable wealth without compromising the standard of living.

1. Calculate True Take-Home Pay and Taxes

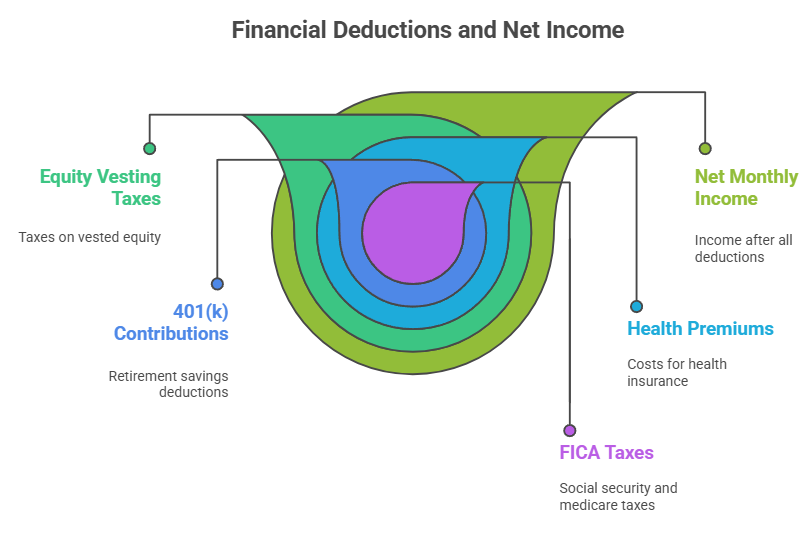

In the case of high earners, it is the calculation of the exact amount of net income after deductions that serves as the groundwork for effective budgeting. The gross income can be misleading since taxes and pre-tax contributions cause a significant decrease in the spendable income. As an example, a gross salary between $200,000 in California which has high taxation levels of up to 37%, after subtraction of federal tax (to a maximum of 37%), state taxation (around 9%–13%), Social Security and Medicare (FICA), health insurance premium and 401 (k) plans would result in a net take-home pay of about $11,000-$12,000 per month. In case the person, too, is a recipient of equity remuneration like RSU, taxation payment on the dividing dates would have to be factored in, which again affects the cash flow and spending ability. Proper calculation gives achievable budget goals and avers expenditures.

2. Implement a Modified Budget Allocation Framework

The classic budgeting principles (e.g., the 50/30/20 rule) will need to be adjusted to higher earnings. An adapted method would have the following allocation:

- 45%-50% of net income ($5,000- $6,000) to fixed requirements like payment of mortgages, utilities, food, and insurance fees.

- 15%-20% of the remaining amount (i.e.$1,500-$2,000) is allocated to lifestyle and discretionary spending (i.e., travel expenses, dining, entertainment, and luxury).

- 30% to 35% of the difference between wealth-building tools, such as high-yield savings accounts, tax-oriented retirement plans, and diversified portfolios ($3,000-$4,200).

This redistribution shows the need to hasten the increase in savings and investment donations in a bid to maximize the growth in net worth due to more expensive living costs.

3. Automate All Savings and Investment Contributions

The long-term wealth accumulation can only be maintained through automation. It is recommended to maximize the contributions to tax-favored accounts; in 2025, one can make up to $23,500 to a 401(k) and $8,550 to a family Health Savings Account (HSA). Automatic transfers make sure that we start at these limits, and therefore, reduce the possibility of losing employer matching or tax benefits. Something systematic after retirement into taxable brokerage accounts encourages diversification and offers liquidity towards retirement targets like purchasing a home or covering school fees. Planned tax estimations and automation should be considered concerning scheduled bonuses or RSU income to encourage disciplined growth, as well.

4. Manage Equity Compensation Strategically

Equity compensation is a complicated but also growing part of high-income compensation, usually in the form of RSUs or stock options. The following are the best practices that can be considered in budgeting:

- Budget only on sound cash flow, without considering unvested RSUs.

- Use all taxable amounts of RSU examples with a 35%-45% as a 1-year parameter to evade surprise taxation.

- Sell systematically blocks of vested shares to reduce portfolio concentration risk; will maintain equity investments at not more than 10% of total net worth.

- Management of time stock option exercises through integration of tax implications, including the Alternative Minimum Tax (AMT), and the existing market trends, to maximize benefits.

- These approaches minimize financial risk and make sure that equity assets supplement, but do not make the financial plan complex.

5. Limit Lifestyle Inflation Through Conscious Spending

Lifestyle inflation, a situation whereby spending increases with an increase in income, is a major barrier to wealth improvement among many executives and professionals. Since it is natural to take pleasure in better incomes, unrestrained expenditure is likely to suck away future savings. Limit the spending on luxury and non-discretionary expenditures to not more than 20% of net income. Complete quarterly financial audits of spending patterns to gauge spending habits and utilize value-based spending, requirements of meaningful life accomplishment, and not impulse or social influence. Postponement of lifestyle improvements like costly cars or houses until career goals are well determined can lead to capital saved being invested.

6. Build Robust Emergency and Sinking Funds

Earners who also have higher incomes have more complicated career pathways and financial requirements that should be provided with higher emergency reserves. Target to have emergency funds to sustain emergency expenses between 9-12 months amounts to $60,000 to $100,000, depending on the normal cost makeup. Besides a buffer during the change of jobs or unexpected medical situations, sinking funds are used to even out hectic lump sum payments, like property tax bills, insurance payments, charity, or vacations. Dispose of these sums as follows: spend between $500 and $1000 a month on these funds to achieve some stability, but keep lifestyle rather flexible.

Additional Tips for High Earners

- Hire accredited financial planners or tax consultants to deal with complex taxation code provisions, estate planning, and asset protection.

- Have diversified preference of investments comprising equities, bonds, real estate, and other assets like private equity or hedge funds to maximize the returns in terms of risk-adjusted returns.

- Alternatives: maximize charitable donations by clustering them to exceed standard deduction limits to reduce the taxable income, and help charitable causes that are also a personal value.

- Re-examine the budgets that were made a year ago and make adaptations in line with lifestyle changes, inflation, and changes in goals to be in line with long-term goals of building wealth.