7 Key Differences Between ETFs and Mutual Funds in 2025 Every Investor Must Know

Intro

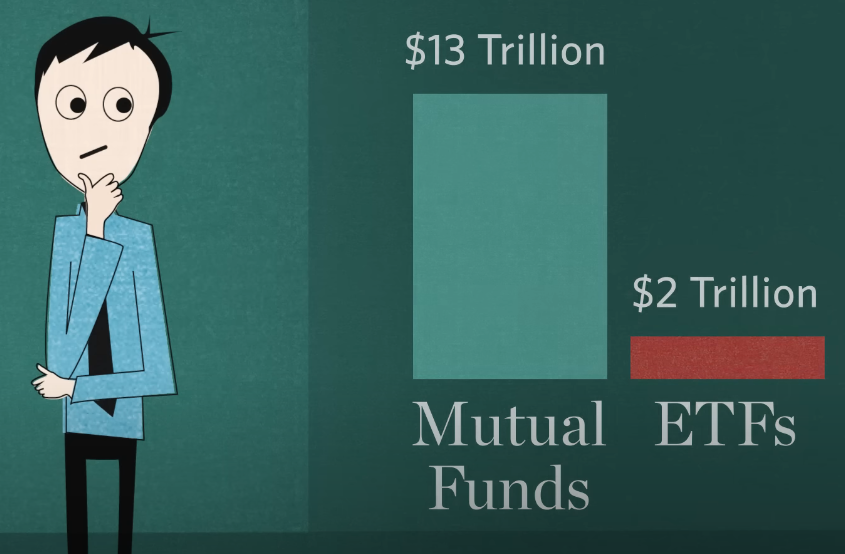

At a single time in 2025, there are an overwhelming number of investment options available to investors in terms of which funds to commit their capital to: exchange-traded funds or old-fashioned mutual funds. They are both pooled investment vehicles, yet the trade, tax, and scale can lead to significantly different portfolio results when employed relative to each other.

1) Trading & Intraday Liquidity ETFs trade like stocks; mutual funds do not

The ETFs are listed on the stock exchange and can be sold or purchased at any time in the market and at market rates. Intraday liquidity allows investors to respond to news, place limit orders, and trade in small steps. In contrast, fund prices have time limitations because they are run once per day at the net asset value (NAV) at the end of the market. This dispersion is important to active traders, tactical rebalancers, or traders who require exact trading.

2) Pricing Transparency: Real-time vs end-of-day valuation

It can be seen that due to their exchange tickers, ETFs are priced. There exists a live price and (fortunately, in many ETFs) an approved indicative NAV throughout the day. NVs are released by mutual funds one day, and therefore, they lack the transparency of real-time value. Three ETFs provide more immediate and transparent paints to the investor of intraday share price moves and spreads.

3) Tax Efficiency ETFs generally distribute fewer capital gains

Tax efficiency has been listed among the most cited effects on a structural level of ETFs. In-kind creation is used in many structures of the ETF, allowing a cut in forced selling and realization of capital gains. According to industry data, there is a wide disparity in the distributions of capital gains of ETFs as compared to capital gains distributions of mutual funds: in 2024, a small portion of ETFs will distribute capital gains in comparison to a significantly greater portion of mutual funds, a difference that investors tend to claim as a comparison of after-tax returns.

4) Costs & Fee Structures Expense ratios, trading costs, and bid-ask spreads

Passive index ETFs, which are managed by large suppliers, are unique in that they are aggressively low on the headline expense ratios. However, don’t forget to add the cost of the trading: Bid-Ask spreads and commission fees (particularly when trading some cheaper ETFs, several brokerage firms will trade them at zero commission). Mutual funds are also more expensive to manage (have a higher expense ratio), and at times a sales load, though the buy/sell spreads do not exist. Comparisons of costs should also encompass a ratio of costs, as well as anticipated trading friction in 2025.

5) Active Management & Product Innovation: active ETFs closing the gap

Historically, ETFs were primarily passive; in 2025, new ETF launches and funds will witness an active influx into the market. Active strategies within ETF wrappers have been provided by many asset managers that provide professional management with the trading and transparency characteristics of ETFs. The move bridges the functionality divide between ETFs and mutual funds (long nature of active management). More options involving the hybrid are in the offing as asset managers become creative.

6) Minimum Investment, Accessibility & Distribution Channels

Administered minimum investment requirements are common in mutual funds (particularly of institutional or retirement share classes), while in-house share classes with low minimum requirements are available in many fund families. The share units of the ETFs are traded on the open markets and are purchased at only the cost per unit share (or part share through brokers). So ETFs are quite convenient among retail investors going through a discount brokerage or an app, compared to mutual fund distribution as used in retirement portfolios and advisor portfolios.

7) Global Adoption & Flows ETFs continue rapid growth, but mutual funds retain niches

ETFTs’ assets and net inflows increased over the past years and benefited from the presence of large net inflows until H1-2025 and high concentrations among key promoters. ETFs have already established themselves as a leading product in North America and scaled in Europe and Asia, although mutual funds continue to dominate in some areas of the retirement market and active allocation vehicles. The latest industry news reveals a strong ETF influx and a booming growth of the ETF product lineup. This has changed availability and investor selection globally.

Practical Takeaways:

- Transparency, intraday trading, and tax efficiency – ETFs can be better.

- As of 2020, dollar-cost averaging with an adviser or some active strategies in a retirement vehicle mutual fund can be more convenient in terms of needing seamless contributions.

- Total cost: ratio of expense + the cost of trading + the impact of tax. Don’t compare headline fees alone.

- Observe active exchange-traded funds when you want a result accomplished by managers within an ETF framework. They represent a rapidly growing population in 2025.

1 thought on “7 Key Differences Between ETFs and Mutual Funds in 2025 Every Investor Must Know”