5 Key Effects of Student Loan Forgiveness 2025

Introduction & Background

In 2025, America will be heading into a new stage of forgiveness of student loans with very different rules and a different political landscape. With millions of Americans continuing to struggle with federal student debt amassing over $1.6 -1.8 trillion, the government’s plan to cancel it will have a ripple effect across the economy.

This analysis focuses on the major changes implemented in the Trump administration and stands as a critical assessment of how those changes will impact the U.S. economy and also on how they will affect borrowers, especially young professionals and families that belong to the middle class

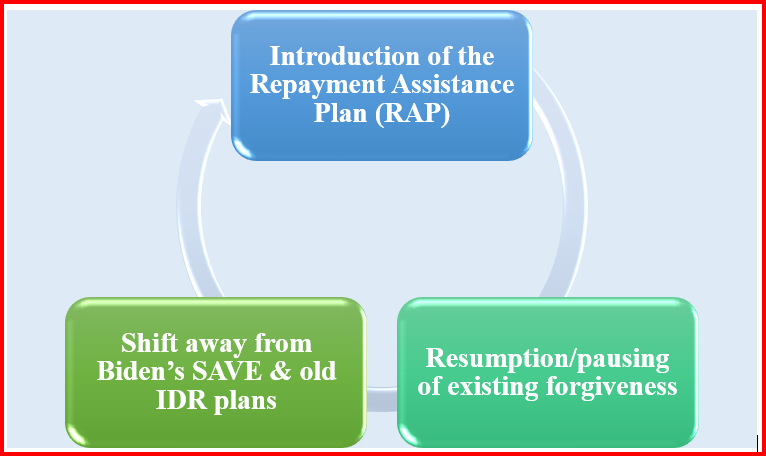

1. What’s New in Forgiveness & Repayment in 2025

Shift away from Biden’s SAVE & old IDR plans

- The SAVE plan of the Biden era was invalidated by a court decision because, according to the court, the Department of Education had overfully exercised its statutory authority.

- Some income-based repayment (IDR) plans, such as SAVE, PAYE, and ICR, are currently being phased out or reformulated under the One Big Beautiful Bill of 2025.

Introduction of the Repayment Assistance Plan (RAP)

- The new legislation provides a new system, the RAP plan, with monthly payments ranging between 1% and 10% of discretionary income, with a fixed payment of $10 monthly. Pardon will be subject to 30 years of qualified payments.

- BORI: Borrowers who fail to implement RAP by July 1, 2026, would default into a regular fixed-repayment term.

Resumption/pausing of existing forgiveness

- A contributing factor was the restoration of forgiveness to income-based repayment (IBR) borrowers who make 20-25 years’ worth of payments by the Trump administration.

- However, this is being held as systems are upgraded to meet legal injunctions on SAVE, leading to delay and uncertainty.

2. Economic Impact: Inflation, Consumer Spending & GDP

Short-term consumer boost

Student-loan forgiveness sets household cash free. As a result, borrowers who previously had to make monthly payments can shift the money to consumption, expenditure on housing, durable goods, and services, and hence, increase consumer spending, which is roughly 70% of the U.S. GDP.

Nonetheless, as the area of forgiveness has now had its boundaries scaled back, to IBR to eligible borrowers with a lag time on it, the net stimulus might be small.

Inflationary pressure & risk

The practice of liquidating the economy is associated with the risk of inflation. When a high number of borrowers spend at the same time, profit levels may become over-demanded compared to supply, thus pushing up prices, particularly in areas like housing, automobiles, and retail sectors.

However, this impact will likely be smaller than that of either fiscal or monetary stimulus. Some of the analyses calculate the relief of typical households to be about 200-300 each month, which would translate to about 100 billion per year in aggregate spending.

Effects on federal budget, deficits, and debt

Mass forgiveness has to be subsidized. Either the government is free to absorb the expenses, and as a result, increase the deficit, or they can shift the burden (e.g., by raising taxes or spending less). Opponents have argued that the relief is skewed to favor more high-earning workers with large debt balances.

It is estimated that the One Big Beautiful Bill will raise deficits and reduce long-term earnings, which, in turn, may reduce the macroeconomic value of forgiveness.

State & local budget effects

States that depend on sales-tax income could be affected when there is a decline in consumption by borrowers. Specifically, the number of states in the extending southern areas is more burdened with student debt in comparison with the state’s personal income.

Reduced levels of default would reduce stress on social safety nets, courts, and state financial aid.

3. Borrower Impact: Gains, Risks & Uncertainty

Who benefits most – and who loses out

- Long-term borrowers are on the verge of forgiveness. Because of the legacy conditions, people with balances could benefit in case they are discharged; however, the forgiveness will be postponed until 2026, and then it will be taxable.

- RAP plan has at least a minimum payment for young borrowers who are new graduates, and this can stretch them over 30 years, extending their financial roll.

- Middle-income households that have moderate levels of debt could have some modest relief, but they also incur the expenses of administrative adjustments.

Risk to credit, delinquency, and defaults

- Recent resume of collections or increased repayment of loans may drive barely surviving borrowers into delinquency. In the case of Generation Z specifically, credit scores are falling, according to FICO reports; the average has fallen by about three points.

- Delays in the processing of forgiveness imply that those borrowers who have already paid their dues are hanging in the air, and they keep paying installments even though they have qualified.

Tax exposure

According to the American Rescue Plan, as of 2025, the federal tax-exempt treatment of forgiven student debt will only last until 2025, by law. Provided that forgiveness is not made until 2026 or later, borrowers will have to pay significant tax on the amounts forgiven. There are already some borrowers who are taxed in such cases; in case relief is not availed, retroactive or special legislation might even be needed.

4. Broader Macroeconomic Risks & Considerations

Policy, legal, and administrative uncertainty

The constant change in policy, like the ruling of courts that prevent SAVE, suspend IBR, and introduce RAP, leaves the borrowers and lenders uncertain. This caution kills the economic signals.

The decreased processing, audits, and oversight can be caused by the reduced capacity in the Education Department because of staff cuts and reorganization.

Moral hazard & equity concerns

Critics argue that blanket amnesty encourages historic risk-taking and punishes those who have already paid off their debts or those who did not take on debt.

Moreover, relief will be skewed towards those who have high-level degrees or earning abilities, e.g., doctors and lawyers, and not low-income borrowers.

Crowding out & fiscal tradeoffs

Widespread relief can restrict the spending capacity of the government in infrastructure development, health, education, and so on. The relief budget could be competing with other priorities in society.

5. What to Watch: Key Indicators & Future Scenarios

- The speed at which it can process forgiveness applications and clear the backlog (PSLF / IBR)

- Tax exemption extended by Congress past 2025.

- Interest rates, inflation information, and changes in consumer spending of groups of borrowers.

- Default and delinquency on student-loan holders.

- Reactions of the credit and bond market to fiscal stress.

- The trends of state-level revenue, especially those that depend on taxes.

One situation: assuming forgiveness is not taxed and is taxed in 2026, a large number of borrowers will have a surprise tax payment, which cancels the benefit.

A different situation: in case the administration simplifies RAP and supports relief through fiscal offset, the macroeconomic stimulus may be greater, but less pronounced compared to complete cancellation.

Conclusion

Student Loan Forgiveness 2025 is a compromise: it is a watered-down, legally limited form of debt relief, not a broad-brush clearing many would have liked to see. It will affect its economy, balancing income, consumption, and relief to some industries, but putting others at risk, and credit strain, and tax surprises. To the U.S. economy, the relief is more of an after-tax cut than a retooling of the economy.

To the borrowers, the decisive factors are time, judicial predictability, and bureaucratic implementation. As a borrower, it is now more important than ever to update your servicer, know timeframes, and what your plan is (IBR versus RAP versus standard).

1 thought on “5 Key Effects of Student Loan Forgiveness 2025”